Lehendabizi, ikus Aurrekontuz hitz bi (1)1 eta Aurrekontuz hitz bi (2)2

Segida:

Bill Mitchell-en article: The non-austerity British Labour party and reality – Part 23

Hona hemen Mitchell-ek aipatzen dituen puntu batzuk:

-

John McDonnell-ek eta Alderdi Laboristak uste dute, ohiko Europako ezkertiar guztiek bezalaxe (barne EH-koek) ezen “we will tax the rich and the crafty tax dodgers to balance the budget”

-

Guzti horiek defizita dela eta, neoliberalen diskurtso bera erabiltzen dute, hots, “they will cut the deficit but it will be a fairer cutting. The rich will pay.” eta Mitchelle-k gehitzen duen moduan, “And pigs might fly.”

Izan ere, zergapetzea dela eta, guztiok gauza bertsua uste dute:

-

Zergapetzeak (edozein izanda haren banaketa) gobernuarentzako dirua biltzen du, zeinak gastua permititzen du. Hauxe da gobernuaren analogia, leku guztietan berbera dela, alegia, gobernua eta familia bat berdinak dira gastuaren kontuaz. Ustea benetan ustel!

- Irakur Mitchell-en Taxpayers do not fund anything

Nahasketa hori dela eta, Mitchell-ek ondoko galderak egiten ditu (ikus linka)4. Baita zenbait erantzun eman ere5.

- Austeritatea bera ez dauka argi McDonnell-ek6

- McDonnell-ek neoliberalen ideologiari segitzen dio, ‘urrezko arau’ari atxikiz7

Argi, DTM-z norbera jabetzen denean, jakitun gara aipatutako denboraren gaineko kostuen eta mozkien parekatzea gezurrezkoa dela8.

Zer ote da kapital gastua?

Demagun zenbait datu:

-

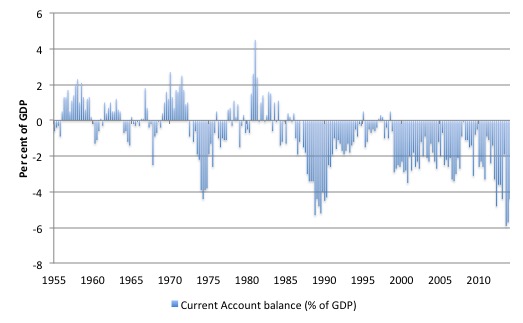

Kanpo balantzea12

-

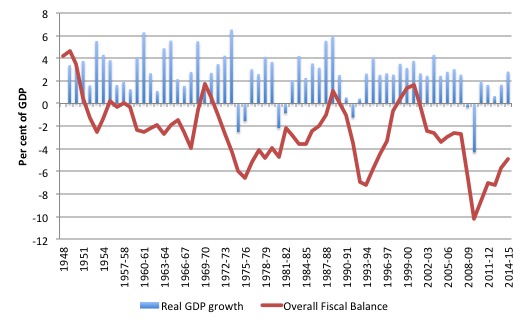

BPG errealaren hazkundea13

-

Balantze fiskal osoa14

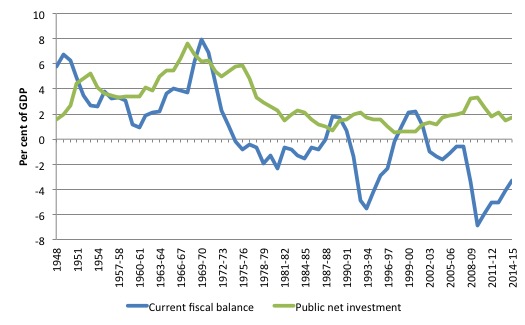

(xiii) Balantze fiskal korrontea eta sektore publikoko inbertsio netoa15

Ondorioa:

Aipatu bezala, ondoko adierazpenak (“deficit denial”, “living within our means”, “getting the budget back into balance”) garrantzirik gabekoak dira, ulertzen baldin baditugu, defizita dela eta, britainiar gobernuaren ahalmenak, moneta jaulkitzailea den aldetik.

Mitchell ezkorra da16, zeren kapital gastua ez baita izango nahikoa inbertsio netoak enplegu osoa sostengatzearren17.

Alderdi Laboristak daukan erronka erabat politikoa da, zeren atrapatuta baitago neoliberalaren tranpa. Austeritatearen aurkakoak izan nahi dute, baina horretarako segitu nahi dituzteneko helburu fiskalek soilik daukate zentzurik baldin eta austeritate jarduera mentalarekin ezkontzen badira, Syriza-k bere buruari jarri zion tranpa bertsua18.

Europako ezker guztiak neoliberalek berek proposatzen dutena errepikatzen du, horretaz jakitun egon zein ez, Britainia Handian bezala, Grezian zein Italian edo Portugalen.

Baina kontuz, ikusi dugun moduan John McDonnell-en proposamenak ez dira Jeremy Corbyn-enak.

(Caveat: Corbyn-ek berak ez dauka oso garbi defizitaren afera. Ikus Mitchell-en Jeremy Corbyn’s ‘New Politics’ must not include lying about fiscal deficits eta Neil Wilson-en Corbynomics and the Current Budget Balance.)

4 Ingelesez: “Is Labour under Jeremy Corbyn going to balance the overall deficit or just the cyclically-adjusted current fiscal balance?

Is Labour under Jeremy Corbyn prepared to maintain levels of public investment that are sufficient to full employ the workforce on an on-going basis and how will he ensure that the public debt ratio would be held at levels below those prevailing in 2016-17?

Has he [McDonnell] really done the sums that will ensure that level of stimulus concentrated on public infrastructure is possible (not in a financial sense but in a practical sense)? I doubt it.”

5 Ingelesez: “I also doubt that an on-going rate of growth in public investment sufficient to smooth the economic cycle and maintain levels of output that would fully employ the workforce is possible. It implies an ever growing public capital goods sector when the reality is that the growth areas will be in personal care services and the tertiary services.”

6 Ingelesez: “What does he actually mean by austerity? The implication he thinks it is a distributional matter – that cutting the fiscal deficit is fine as long as the rich are losing purchasing power and the poor and middle classes lose less purchasing power proportionately) via taxation.

But while austerity has distributional impacts it is not really about equity when macroeconomists use the term.

I touched on this matter (…) Jeremy Corbyn’s ‘New Politics’ must not include lying about fiscal deficits.

Austerity occurs when the government runs deficits that are too small relative to the spending and saving decisions of the non-government sector.

In this context, it is moot where the revenue comes from. The impacts of running insufficient fiscal deficits usually does impact on the poor and disadvantaged, most notably, because it causes mass unemployment and/or underemployment. And I don’t diminish the concern we should have for those distributional consequences.

But from a macroeconomics perspective that is not the point. Austerity is about the sufficiency of the deficit contribution to total spending and national income generation.

So in what sense is a fiscal balance of zero appropriate?

Britain will not generate large external surpluses in the foreseeable future, which means the only way that the private debt situation can be brought under control without driving the economy back into recession, is for the government to increase its fiscal deficit.

Now if they plan to balance the ‘current’ fiscal position, then all the work has to be done by the capital component. That imposes a rigidity that might be impossible to maintain and ensure effective use of public resource utilisation.

How does Jeremy Corbyn propose that Britain will create external surpluses that are of sufficient magnitude to meet the desires of the private domestic sector to net save, while at the same time, ensuring overall spending is sufficient to achieve full employment and allow the government sufficient spending scope to provide first-class public services and robust public infrastructure development?

Given history and the current circumstances, I would think an on-going fiscal deficit – larger than it is now – is the correct strategy if the well-being of the British people is to be advanced.

But where the plan fails is that I do not think the capital fiscal balance can do all the work. Further, there is no inflation anchor in this sort of approach.

What happens if the necessary net spending in the economy sufficient to generate full employment is beyond the capital goods sector’s capacity to supply the necessary output and employment to meet the on-going growth in public investment spending? Well inflation happens and John McDonnell presents no solution to that problem.

There are many problems with the use of the ‘Golden Rule’, which effectively John McDonnell claims Labour will sign up for – a la Gordon Brown.”

7 Ingelesez: “The one advantage is that public investment expenditure does not have to be used in a counter-cyclical manner – cutting when non-government activity is declining – to meet pre-conceived fiscal balance targets.

The cuts to public investment in the 1990s in many European countries as they struggled to meet the convergence criteria that would allow them to enter the final stage of the shift to the common currency were particularly damaging.

It not only undermines current economic activity and pushes up unemployment but by slowing the rate of capital accumulation it also undermines the future growth potential.

In political terms, it is much easier to cut capital expenditure than current expenditure, the latter being more directly noticable for voters on a daily basis (pensions etc).

So within the neo-liberal cutting ideology, the Golden Rule thus might remove the bias against public investment.

But then why isn’t Labour rejecting this ideology outright and educating the public about the capacities of a currency-issuing government and the opportunities those capacities provide?

Proponents of the Golden Rule also appeal to its equity advantages whereby the public expenditure is steadily finances over time as the debt is repaid, which means there is a better matching of who receives the benefits from the services flowing from the infrastructure and who pays for it.”

8 Izan ere, “The true ‘cost’ of providing public infrastructure is not the flow of financial outlays (including interest payments) over time but the real resources that are deployed to construct and maintain the infrastructure.

For most projects, the cost is mostly incurred upfront in the construction phase, which means the current or near generations still end up bearing most of the costs.”

9 Ingelesez: “Then we get into demarcation issues as to what should be classified as net investment spending. While the split between current and capital is normally defined as some time period in which the benefits of the spending are exhausted (less than or more than 12 months usually), it is more sensible to think of capital expenditure as that which improves the potential productive capacity of the economy.”

10 Ingelesez: “MMT conceives of productivity much more broadly than the narrow concept that neo-liberals focus on. Productivity is not just the contribution an input makes to the private profit bottom line.

(…) productivity is a very broad term in my view.

This leads me to suggest that the definition of productive capital should also be very broad? One could make a strong case to include much of the spending on health, education, research and development along with spending on bridges, transport and other physical capital.

For example, the public investment in the education of its population delivers massive social and private returns over the person’s lifetime. Why is that not capital expenditure?

If education and health expenditure on teachers and nurses and libraries and books, for example, are considered as current spending, then the Golden Rule biases total public spending against it in favour of ‘building bridges’, which might be a poor use of the society’s real resources.

The bias towards physical infrastructure and financial assets is reflected in what governments put in their so-called financial statements – specifically their balance sheets or statements of financial position.”

11 Ingelesez: “Neo-liberal commentators use this information to judge, according to their faulty logic, whether a government is insolvent or not. This approach is just another string in their anti-government bow, which builds on the deficit and debt hysteria.

Two aggregates are assembled – net worth and net financial worth. The former is the difference between total measured assets and liabilities.

What sort of assets are included? Public land and buildings, infrastructure, plant and equipment, etc. The liabilities typically include outstanding government debt, future liabilities (for example, superannuation for government workers).

They use net financial worth as a measure because many physical assets cannot be easily sold for cash. This measure is the one that commentators use to judge the so-called ‘financial viability’ of government.

(…)

The conservatives claim that this signals that the government is insolvent because if it liquidated all its assets it would still not be able to meet its liabilities.

But of course, the government is not a household nor is it a financial corporation – both of which are always financially constrained in their spending.

The British government could liquidate all its liabilities whenever it wanted to – although such an action would not be sensible. But the capacity is there to do it.

Even the conservatives admit that a government is not a corporation – because according to them it has the taxation powers. They then wade in with their usual nonsense about the damages of taxation.

The point is that if Labour broadened what it would consider to be capital expenditure then the Golden Rule is less rigid than otherwise.

The whole framework is based on a false notion that taxes and bond-issuance fund government spending. But even with that obvious observation, Labour could overcome some of the obvious problems of relying on capital infrastructure spending to drive the necessary growth to keep the current balance at zero and maintain full employment.

But then they would not have a chance of keeping the public debt ratio below the 2016-17 level, given McDonnell is committed to issuing public debt to match the capital deficit.

He could get around that by avoiding debt issuance altogether and instructing the Bank of England to honour all cheques HM Treasury issues but if they are prepared to embrace that then they should just be able to abandon the whole charade and admit that the deficit (current, capital, whatever) is a ridiculous financial balance to target and obsess about.”

12 Ingelesez: “… the following graph shows the external balance (as a per cent of GDP) for Britain from 1955 to 2014. Prior to the OPEC oil crisis, Britain usually ran an external surplus with exceptions. This was true even if we went back to the 1920s, bar the Second World War period.

This means that after the mid-1970s, for the private domestic sector to save overall, the public sector had to be in deficit overall of varying magnitudes.”

13 Ingelesez: “...the following graph, which shows average annual real GDP growth since 1948.

The numbers corresponding to the decades (1950s etc) are the average growth rates for the periods. The last entry is from 2010 to 2014.

The pattern shown is similar for most advanced nations. The Post World War II period initially spawned high real GDP growth rates with strong productivity growth and real wages growth. National government fiscal deficits were the norm and supported strong private spending and saving patterns.

That all came to an end once Monetarism antagonism to fiscal activism took hold in the 1970s and deregulation was pursued, first with large-scale privatisation, then attacks on the unions, and then full-scale financial market and labour market changes.

The growth performance of the economy started to slide (as did productivity growth). As the neo-liberal policy mentality firmed in more recent decades growth took a further step downwards and politicians claim success at growth rates that are nearly 50 per cent below what was the norm during the Keynesian period.

The period since 2010 in the UK has been a relative disaster in this sense.“

14 Ingelesez: “The next graph shows the overall fiscal balance (the sum of the current and capital balances) as a per cent of GDP since 1948 for Britain (red line) and annual real GDP growth (blue bars). The GDP growth is not aligned against financial years in Britain (March to April) which alters the perception of lags a little but to no great extent.

The fiscal balance is written as Total Public sector receipts minus total public sector expenditure and so a positive number is a surplus.

You can see the in the Government achieved a fiscal surplus in 1969-70 and a declining surplus in 1970-71 (…)

That surplus was short-lived and a major recession followed in 1974 and 1975.

Recession also soon followed the next period of fiscal surplus under the Chancellorship of Nigel Lawson and the financial crisis followed Gordon Brown’s fiscal squeeze.

These surpluses were recorded as the external deficit was increasing, which meant they were also associated with rising private domestic indebtedness.

The accumulation of that position ultimately has caused the period of appalling economic performance since the GFC. The real GDP growth that was recorded under Brown’s period as Chancellor was driven by unsustainable private debt accumulation.”

15 Ingelesez: “The next graph then shows the Current fiscal balance for Britain (as a per cent of GDP) and Public sector net investment (as a per cent of GDP) since 1948.

Two things are very obvious.

1. Public net investment as a share of the economy has fallen dramatically in the neo-liberal years (as discussed above it was easier to cut than current spending). This drop has coincided with the slow down in real GDP growth and has, in part, caused that. The damage of the Thatcher sea-change.

2. The current fiscal balance has fluctuated substantially but is now substantially in deficit.

So a case can be made that John McDonnell has a fair amount of ‘room’ to operate in given how low the public investment ratio is. But if he is also wanting to reduce the public debt ratio (as per the ‘Charter of Budget Responsibility’) then the scope is extremely limited, especially as he will have to keep issuing debt to match the current deficit that he will inherit later in the decade if elected.

But then he also will have a major job on his ‘non-austerity’ hands if he thinks he can drive growth fast enough or tax the rich hard enough to close the current fiscal deficit without cutting current spending significantly.”

16 Ingelesez: “I doubt they will be able to achieve sustained growth, full employment, stable inflation, a balanced current fiscal position and keep the public debt ratio stable or reduce it.”

17 Ingelesez: “I do not think the capital expenditure opportunities exist to rely on ever increasing growth in public net investment for sustaining full employment.”

18 Ingelesez: “The real challenge facing British Labour is the political one that they have been caught in the neo-liberal framing trap. They want to be anti-austerity but they also want to pursue the fiscal targets that only make sense if one is wedded to the austerity mindset.

It is starting to look like the trap Syriza set for itself – anti-austerity yet stay in the Eurozone. That couldn’t be done politically.”