(Euskal progre guztientzat -ekonomialari, politikari, kazetari, …- ea zertxobait ikasiko duten!)

Eric Tymoigne(e)k Bertxiotua JP Koning

Maybe time to finally learn that inflation is about the rate of spending not about monetary policy, monetary financing, etc.

Eric Tymoigne(e)k gehitu du,

The Bank of Japan can’t increase inflation because the government is obsessed with deficit reduction: http://andolfatto.blogspot.ca/2016/11/the-failure-to-inflate-japan.html … from @dandolfa

2016 aza. 29

David Andolfatto-ren The failure to inflate Japan3

(i) Sarrera4

(ii) Japoniako Bankua, alegia, banku zentrala5

(iii) Eszeptizismoa6

Autoritate fiskala7

(v) Bonoen afera: QE eta inflazioa8

(vi) Inflazio tasa9

(vi) Japoniako gobernua eta zor publikoa10

(vii) Japoniako gobernua eta defizit murrizketa11

(viii) Japoniako gobernua eta austeritatea12

(ix) Gobernua, bonoen erosketa eta inflazioaren helburua13

(x) Japoniako Banku zentrala14

Ondorio gisa15:

“IF the monetary and fiscal authorities wish to implement a 2% inflation target, THEN success of the policy (in present circumstances) requires a sufficiently accommodative fiscal policy (deficit financed expenditures and/or tax cuts) when inflation and inflation expectations are running below target. “

Additional readings:

[1] Understanding lowflation

[2] A model of U.S. monetary policy before and after the great recession

Euskarazko gehigarriak:

PQE (politika fiskala) eta QE (politika monetarioa)

Likidezia monetarioa(ren operazioak) eta politika fiskala(ren parte hartzea)

EBZ, Draghi, tasa negatiboak eta politika fiskala

Politika monetarioa efektiboa izateko, batera lan egin behar du politika fiskalarekin

Ekonomialariek eta politikariek ez dute ikasi nahi

4 Ingelesez: “On January 22, 2013, the Government and the Bank of Japan issued a rare joint statement on overcoming deflation and achieving sustainable economic growth. The purpose of the statement was to introduce a two percent inflation target. It was issued jointly to emphasize that the monetary and fiscal authorities could be expected to coordinate for the purpose of achieving their shared goal–a clear attempt to enhance the credibility of the new inflation target.”

5 Ingelesez: “On April 4, 2013, the BOJ explained how it intended to achieve the inflation target: Quantitative and Qualitative Easing. QQE is (more or less) standard monetary policy, except on a larger than normal scale. That is, the policy entails the creation of bank reserves (money) which are then used to purchase securities–primarily government bonds (JGBs).”

6 Ingelesez:”At the time, I was skeptical that the policy would work as intended (see here). My skepticism has not abated since then. This post is about explaining why. In a nutshell, my argument is that while the BOJ seems willing to increase inflation, it is largely unable to–and while the government is able to increase inflation, it seems unwilling to. In short, the necessary policy coordination appears to be absent.”

7 Ingelesez: “Let’s begin with some basics. First, note that a JGB is basically an interest-bearing claim to (possibly) interest-bearing BOJ money. The total nominal government debt is the sum of BOJ money and JGBs. The fiscal authority controls the total supply of debt. The monetary authority determines its composition (between money and bonds). Quantitative easing increases the supply of money and reduces the supply of bonds held in the wealth portfolios of private agents. That is, it changes the composition of government debt without changing its level.”

8 Ingelesez: “Because bonds are normally discounted (that is, they generally earn a higher yield than money), an open-market operation that alters the composition of government debt will generally have real and nominal consequences. But in present circumstances, the yield and risk characteristics of Japanese money and bonds are very similar. In the limiting case where money and bonds are perfect substitutes (we’re not quite there yet), altering the composition of government debt (without affecting its level) is inconsequential. It’s like swapping one hundred dollars worth of $10 bills for one thousand $1 bills. Such an operation–even it is permanent–is not likely to have any measurable effect on the economy, including the price-level. Why should it? Empirically, it didn’t seem to have any measurable impact on inflation the first time Japan tried QE from 2002-2006 (see also my 2003 paper here, section VI).”

9 Ingelesez: “For the rate of inflation to rise, one of two things must happen: [1] the growth rate in the supply of nominal government debt must rise; or [2] the growth rate in the demand for government debt must fall.

One interpretation of what has happened in Japan (and elsewhere) is that a persistently bearish sentiment has led to an elevated growth in the demand for safe securities, like JGBs (at the expense of private investment). The effect of this force is to drive down bond yields and create deflationary pressure (deflation is a market mechanism for increasing the growth rate of the real quantity of nominal object when it is in short supply.) While the supply of nominal debt has been rising, ultra-low bond yields and lowflation suggest that the demand for debt has been rising even more rapidly.

According to the joint statement mentioned above, the government’s commitment to helping the BOJ achieve the 2% inflation target amounts to reducing the demand for government debt by implementing reforms intended to create a bullish investment climate designed to stimulate real economic growth (the third of Abe’s three arrows). While this is fine as far as it goes, what’s the contingency plan in case the third arrow cannot be released or misses its mark?

In my view, the appropriate contingency plan would involve a promise to use nominal debt to finance (say) social security payments or tax cuts as long as inflation remains below target. This is essentially “helicopter money.” The “money” in this case is government debt (whether the BOJ monetizes new debt or not is irrelevant if the two objects are perfect substitutes). Importantly (and as far as I understand), the BOJ has no authority to engage in helicopter money. Only the government can do this. And in present circumstances, my view is that only a commitment on the part of the government to adjust money/debt-finance expenditures to meet the inflation target can render it credible. The question is whether the government has expressed any willingness to support the inflation target in this manner. All the evidence I can find suggests that the answer is no.”

10 Ingelesez: “To begin, the Japanese government appears to be very concerned with the size (and growth) of its public debt. From the joint statement above:

In addition, in strengthening coordination between the Government and the Bank of Japan, the Government will steadily promote measures aimed at establishing a sustainable fiscal structure with a view to ensuring the credibility of fiscal management.

Now don’t get me wrong–everyone agrees that a “sustainable fiscal structure” is a good thing. The question is in determining what is sustainable. Of course, the debt-to-GDP ratio cannot rise forever. But it may certainly rise to a much higher level, even from its current elevated position, especially in light of how low interest rates presently are.”

11 Ingelesez: “The government of Japan, however, appears almost obsessively concerned with deficit reduction. Publications from the Ministry of Finance seem to go out of their way in raising debt-sustainability alarm bells. Consider the contents of this Japanese Public Finance Fact Sheet, for example. Most of the document stresses the need for “fiscal consolidation” (deficit reduction) and includes lessons to be drawn from the European debt crisis. The graph of total government expenditure on page 4 strangely includes spending on the repayment of debt. And on page 3, there is the familiar and misleading “here is what a family’s balance sheet would look like if it behaved like the government” exercise. This is a great way to promote the government’s seriousness about stabilizing the debt-to-GDP ratio. But it is not, in my view, a policy that is consistent with helping the BOJ achieve its 2% inflation target.

And by the way, just how serious is the government debt problem in Japan? Japan’s debt-to-GDP ratio is presently 250%, or so we are told. As it turns out, this figure overstates the level of public debt (see here, section 3.1). The 250% figure represents gross debt, which includes government loans and certain intragovernmental transfers, all of which should be netted out. Once this is done, the net debt-to-GDP ratio is closer to 150%.”

12 Ingelesez: “Moreover, if one further accounts for the sizable quantity of government assets, the ratio falls to 100% (see the balance sheet of the central government here on page 51). And finally, if one was to view the fact that 40% of government bonds are held by the BOJ and likely to remain monetized, the ratio falls further still. In my view, the very low yield on JGB’s reflects the market’s assessment that public finances in Japan are nowhere near being out of order (a caveat to this view here).

So, relative to the market demand for their product, the government of Japan appears to be in “austerity” mode–it is bent on limiting the supply of highly-valued JGBs. In the meantime, the BOJ is aggressively purchasing the limited supply of JGBs to the point where it is now worried that the supply of bonds available for purchase will soon be exhausted (story here).”

13 Ingelesez: “How can the BOJ credibly promise to continue with its bond purchases until its inflation target is met? It can’t. Not without the proper support from the government, which appears not to be coming anytime soon. And so, after a transitory blip in inflation following the austerity-induced VAT, headline CPI is back near zero territory.”

14 Ingelesez: “Partly out of a concern over running out of eligible securities to purchase, the BOJ recently announced a new negative interest rate policy (NIRP) with yield curve control (YCC); see here. The intervention appears to have little impact on inflation expectations (inflation and inflation expectations today are similar to the early 2000s, prior to the financial crisis).”

15 Ingelesez: “Let me conclude. First, this post is not meant as an argument in favor of the 2% inflation target. Second, it should not be construed as an argument against the Japanese government’s debt management strategy. Nor is it an argument against the BOJ’s asset purchase program. I will discuss these issues in a subsequent post.

The point of this post is as follows. IF the monetary and fiscal authorities wish to implement a 2% inflation target, THEN success of the policy (in present circumstances) requires a sufficiently accommodative fiscal policy (deficit financed expenditures and/or tax cuts) when inflation and inflation expectations are running below target. Absent this commitment on the part of the fiscal authority, the endeavor is ultimately doomed (if an overall bearish outlook persists) and–as a consequence–the credibility of a monetary authority that keeps promising an inflation it cannot deliver may at some point be jeopardized.”

joseba says:

Japoniako Bankuaz: DTM, bono-merkatua, inflazioa

Bill Mitchell-en Bank of Japan once again shows who calls the shots

(http://bilbo.economicoutlook.net/blog/?p=40250#more-402509)

On August 1, 2018, the 10-year Japanese government bond yield, shot through the roof (albeit a very low one). Yields shifted from 0.05 per cent on July 31 to 0.129 on August 1, which was the largest one-day rise since July 29, 2016 (when the yield rose 0.101 per cent). The Financial Times article (August 1, 2018) – Japanese bond market jolted as traders test BoJ resolve – wrote that “traders wasted no time in testing the Bank of Japan’s resolve to loosen its target range for the debt benchmark”. So what was that all about? And what key point does it demonstrate that seems to be lost on mainstream economists who continually claim that government debt is, or can become a problem once bond markets demand higher yields? The Japanese bond market has shown once again that private bond traders cannot set yields on government bonds if the central bank intervenes. Next time you hear some mainstream economist claiming a currency issuing government is running deficits at the will of the investors (read bond markets) politely tell them they are clueless. Japan once again provides the real world Modern Monetary Theory (MMT) laboratory – every day it substantiates the underlying insights contained within MMT and refutes the core mainstream propositions. The bond market over the last month or so demonstrates that the Japanese government is increasingly net spending by using credits created by the Bank of Japan, whatever else the accounting structures might lead one to believe. With inflation low and stable, these dynamics surely put paid to the various myths that a currency-issuing government can run out of money and that central bank credits to facilitate government spending lead to hyperinflation.

I last wrote about the dynamics of Japan’s bond markets in this blog post – More fun in Japanese bond markets (February 7, 2007).

For further background, see this blog post – Bank of Japan is in charge not the bond markets (November 21, 2016).

Essential summary points:

1. If the demand for government bonds declines, the prices in the secondary market decline and the yield rises (see blog link above to understand why).

2. Once bonds are issued by the government in the ‘primary market’ (via auctions) they are traded in the ‘secondary market’ between interested parties (investors) on the basis of demand and supply. When demand is strong relative to supply, the price of the bond will rise above its ‘face value’ and vice versa when demand is weak relative to supply.

3. Any central bank has the financial capacity to dominate the demand for any specific maturity bond in the secondary markets and thus can set yields.

Those who follow Japanese economic policy shifts will know that the Bank of Japan has been trying to push the inflation rate up for many years.

The most recent attempt started on April 4, 2013 when its QQE bond-buying extravaganza was resumed.

Since then this policy has morphed into an even more ‘easy’ money policy initiatives – October 31, 2014 they revved up QQE, then introduced their Negative interest rate decision on January 29, 2016, and then on September 21, 2016, they introduced their yield curve control decision.

I outline those policy shifts in detail in the blog posts cited previously.

The point is that these monetary policy gymnastics have been largely unsuccessful. The spike in inflation you can see in 2014 was due to fiscal policy (consumption tax hike), which should tell you something about the relative strength of each of the two aggregate policy instruments (monetary and fiscal).

The point is that the Bank of Japan is now in a position of its own making.

Having sworn that it would maintain its bond-buying program until inflation was in the 2 per cent range and with the Governor Haruhiko Kuroda suggesting in a – Speech to the Foreign Correspondent’s Club of Japan – on March 20, 2015 that “CPI inflation is expected to reach 2 percent in or around fiscal 2015”, the policy is being extended well beyond its initial scope.

They are under attack from the banksters and speculators who are unable to make larger profits with long-term yields around zero.

This graph shows the 10-year JGB yield from June 1, 2018 to August 30, 2018, with the spike on August 1 noticeable.

The games started the week before when the 10-year JGB yield rose on July 23, 2018 by 0.052 points. That was a precursor to the larger rise on August 1.

The largest single-day rise in 10-year JGB yields occurred on May 15, 1987, when yields jumped from 3.492 per cent to 3.83 per cent.

Speculation was rife that the BoJ would relent on its “QQE with Yield Curve Control” program and start allowing yields to rise.

There has been no shifts in inflationary expectations or, for that matter, bid-to-cover ratios (which might indicate that investors are increasing risk attached to these assets).

It was a case of the usual “unnamed sources” telling Reuters that the policy had to ease even further – see their news report (July 21, 2018) – Exclusive: BOJ to debate policy change in July to make its stimulus sustainable: sources.

The changes foreshadowed related to whether the bond-buying program was “sustainable” (Reuters word) given that it was likely that the inflation target of 2 per cent would take much longer than previously estimated to reach.

Reuters quoted a “source” who “declined to be identified” (meaning I usually disregard) as saying that the “cost of prolonged easing is becoming ‘hard to ignore’”.

Which you should read as saying the investors are annoyed that yields are being held at zero by the BoJ and want more amplitude to help them in their speculative behaviour.

The Reuters’ Report lists the investor concerns:

1. “The BOJ could tweak its yield-curve control (YCC) programme to allow for a more natural rise in long-term interest rates to ease the pain on banks from years of near-zero rates, they say”.

Which raises the questions as to why the debt is being issued in the first place. Who benefits? Obviously the banks want to return to the days where they could get risk-free annuities flowing to them from JGBs (aka corporate welfare).

2. “the bank’s huge purchases are drying up market liquidity and distorting price action” – meaning that the issuance of the JGBs is more about providing speculators with a risk-free asset which they can use as a benchmark to price their own risky assets and seek haven in when uncertainty increases (aka corporate welfare).

3. “the rising cost of prolonged easing, such as the strain on bank profits” (aka corporate welfare).

The reality is that the BoJ would face a huge credibility problem if it abandoned its zero-rate YCC policy with the key inflation rate measure still a long way from reaching the 2 per cent target.

How could they justify it other than as a sop to corporate Japan?

On July 31, 2018, the Bank of Japan released a statement – Strengthening the Framework for Continuous Powerful Monetary Easing – which provided the latest information from the Monetary Policy Meeting on its policy stance:

The announcement said that:

… the Policy Board of the Bank of Japan decided to strengthen its commitment to achieving the price stability target by introducing forward guidance for policy rates, and to enhance the sustainability of “Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control.”

Accordingly:

1. “The Bank intends to maintain the current extremely low levels of short- and long-term interest rates for an extended period of time”.

2. “The Bank will apply a negative interest rate of minus 0.1 percent to the Policy-Rate Balances in current accounts held by financial institutions at the Bank” – so a tax on reserves.

3. “The Bank will purchase Japanese government bonds (JGBs) so that 10-year JGB yields will remain at around zero percent” and in a footnote they said “In case of a rapid increase in the yields, the Bank will purchase JGBs promptly and appropriately.”

That footnote tells you everything really. I will come back to it.

4. “the Bank will conduct purchases in a flexible manner so that their amount outstanding will increase at an annual pace of about 80 trillion yen”.

5. There were some changes in the way the BoJ deals with purchases of non-government bonds.

6. The other statements confirmed it was committed to maintaining its “QQE with Yield Curve Control” but would do so in a “more flexible manner” so as to reach a “price stability target of 2 percent a the earliest possible time, while securing stability in economic and financial conditions.”

Bloomberg reported that the ‘market’ considered that statement meant that the BoJ would “double” the permitted fluctuations in the 10-year bond yield from “0.1 percentage point on either side of 0 percent” to 0.2 per cent.

That is also what the FT article (August 1, 2018) – Japanese bond market jolted as traders test BoJ resolve – had reported, viz … “The central bank doubled the level it will permit 10-year yields to climb from 0.1 to 0.2 per cent”.

As a result the yields started moving about as the bond traders ‘tested’ the BoJ “resolve” (FT words).

One market trader, quoted in the FT article interpreted the developments in this way:

The message Kuroda was keen to give was to allow a wider movement in 10-year bonds but that doesn’t mean he’ll allow it to drift … The market is now going to find out what it can get away with.

That statement is very significant.

When I child tests their parent’s resolve to see what “it can get away with” it demonstrates who has the power in the relationship.

It is the same with the relationship between bond markets and central banks. The former operates within the space granted to them by the policy decisions of the latter.

The central bank always calls the shots on yields and the bond markets only set yields if the government allows them to.

This should tell you that all the claims made by mainstream economists and the sycophantic commentators that just copy their words that bond markets will drive yields up when they lose trust in a government’s ability to pay and this sparks a crisis which can only be resolved by fiscal austerity are hollow.

The bond markets can never drive a currency-issuing government into insolvency.

The bond markets can never drive yields up to elevated levels unless the government (via its central banks) allows that.

The bond markets are mendicants in this context.

And it didn’t take long for the JGB speculators to learn the lesson – again.

Just two days after the MPC met (July 31, 2018), the BoJ launched a so-called “special buying operation” (outside schedule), which stopped the rising yields in their tracks.

This demonstrated that the speculation in the week or more before that the BoJ would allow the fluctuations in 10-year bonds to double was folly.

On August 2, 2018, the Deputy Governor of the BoJ told journalists that “If yields rise rapidly, the bank will purchase JGBs promptly and appropriately” (Source).

The graph above (10-year bond yields) shows that the BoJ is maintaining a slightly wider yield margin under its yield curve control and QQE program but not as large as the financial markets desire.

Mainstream economists eschew this sort of strategy and claim that the central bank can only achieve this outcome if the targeted yields are consistent with what the bond markets want anyway.

That is, of course, a false claim.

In reality, the only consequence of a discrepancy between the targeted yields and the market expectations of future yields held by bond traders would be that the central bank would eventually own all of the bonds in the target range.

There would be no problem arising from that eventuality.

The bond traders might boycott the issues and force the central bank to take up all the volume on offer. So what? This doesn’t negate the effectiveness of the strategy it just means that the private buyers are missing out on a risk-free asset and have to put their funds elsewhere. Their loss!

Eventually, if the government bond was the preferred asset the bond traders would learn that the central bank was committed to the strategy and would realise that if they didn’t take up the issue the Bank would.

The Bank of Japan’s current policy is demonstrating that it runs the show not the bond markets.

To repeat the reality again:

1. The Japanese government can never run out of money (yen). It is impossible. Therefore it can never become bankrupt.

2. The Bank of Japan can maintain yields on JGBs at whatever level it chooses, at whatever maturity range it targets, and for as long as it likes. The bond market investors are incidental to that capacity and are supplicants rather than drivers.

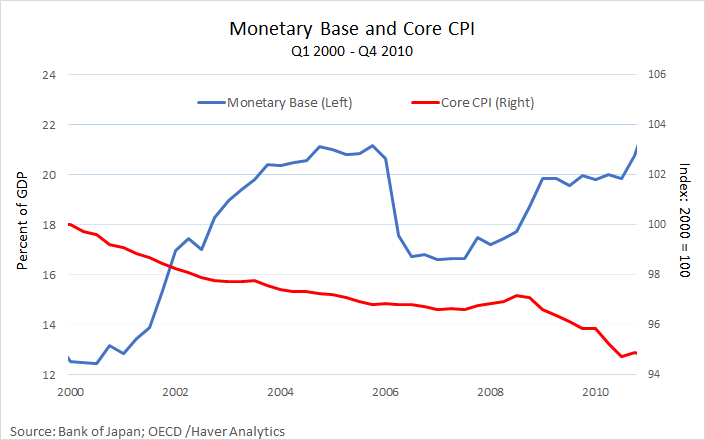

3. The size of the Bank of Japan’s balance sheet (monetary base) has no relationship with the inflation rate.

4. If the Bid-to-Cover ratios at bond auctions fell to zero – that is, private bond dealers offered no bids for an auction – then the government could simply instruct the Bank of Japan to buy the issue. A simpler accounting device would be to stop issuing JGBs altogether and just instruct the Bank to credit relevant bank accounts to facilitate the spending desires of the Ministry of Finance.

5. If private investors choose to buy other assets once the risk in international markets subsides then the Japanese government (the consolidated central bank and treasury) could just buy more of its own debt – to near infinity.

Please read the following blogs – Building bank reserves will not expand credit and Building bank reserves is not inflationary – for further discussion.

Here is my latest ‘surface’ graph for Japan for the period July 1, 2018 to August 31, 2018.

For readers unfamiliar with reading surface charts of yield curves, the vertical axis shows the yields (depicted in the coloured legend at the bottom of the graph). The horizontal axis shows the maturity of the debt instrument issued from 1-year to 40-year JGBs.

The depth axis shows the date span covered.

In the shorter maturities JGBs, there is remarkable stability across this period with the negative interest rate policy being maintained.

Investors are providing loans to the Japanese government at negative rates righ up to the 7-year maturity.

You can also see the ripples across most maturities at the end of July, coinciding with the ‘testing’ period.

And then once the BoJ reasserted its position and the fluctuation range was clearly lower than the markets hoped for, the surfaces became stable again.

Increasing Bank of Japan holdings of Japanese government debt

To further accentuate the point that the central bank calls the shots, the following graph shows the proportion of total national government debt in Japan that is held by the Bank of Japan from January 1990 to June 2018.

The secondary JGBs market has been very thin since the QQE program began and sellers in that market have declined.

Why? Because as the auction yields have gone negative, current bond holders who purchased the debt instrument at positive yields, will worry about having funds (from sales) which are only going to attract negative returns (losses). The smart strategy in that case is to maintain long positions.

In February 2011, the Bank of Japan held 7.1 per cent of all the outstanding JGBs (across most maturities). By September 2016, that ratio has risen to 47.4 per cent and will rise further as the QQE program continues.

Since the April 2013 announcement, the monetary base has risen from 1,495,975 trillion yen to 4,976,398 trillion yen (as at end June 2018).

Where is the accelerating inflation? Answer: in flawed Monetarist textbooks!

Since the April 2013 announcement, bank reserves have risen from 595,334 trillion yen to 3,444,126 trillion yen.

Where is the boom in bank lending? Answer: in flawed mainstream monetary textbooks!

The monetary operations really just mean that the Japanese government is spending by using credits created by the Bank of Japan, whatever else the accounting structures might lead one to believe.

With inflation low and stable, these dynamics surely put paid to the various myths that a currency-issuing government can run out of money and that central bank credits to facilitate government spending lead to hyperinflation.

Conclusion

Once you appreciate the fact that the central bank can control government bond yields at any level it chooses, the next step in the transition is to realise that such interventions are, in fact, redundant.

The best thing that a sovereign government can do is consolidate its treasury and central banking operations (make them consistent in a policy sense) – which would make macroeconomic policy totally accountable to voters unlike today where the central bankers do not face election.

Then the treasury should net spend as required to ensure that the economy achieves and sustains full employment and price stability. This may under some circumstances (very strong external surpluses) require a fiscal surplus, but normally for most countries it will require continuous fiscal deficits of varying proportions of GDP as the overall saving desires of the private domestic sector varied over time.

The treasury should issue no debt at all. Even those who argue that the government should issue short-term paper to allow the central bank to reach its target interest rate via liquidity management operations now realise that interest payments on excess reserves accomplishes the same end.

All those commentators who claim that accelerating inflation would result if governments abandoned debt-issuance but continued to run deficits have been repeatedly shown to be wrong.

No increased inflation risk would be introduced by the government refraining from issuing debt to match any fiscal deficits it might be recording. The monetary operations that accompany fiscal policy changes have very little impact on increasing or decreasing the inflation risk of continuously running an economy close to full capacity. The risk is real but can be managed.

Further, there is no financial reason for issuing the debt because the sovereign government retains monopoly control over the currency. The practice of debt-issuance is a hang-over from the gold standard era where governments had to fund their spending in order to retain control over the exchange rate.

The practice has lingered because it is now a convenient ideological cum political tool used by neo-liberals to limit the size of government and to give the corporate sector access to corporate welfare (the risk-free government debt) that they use to create profit.

If everyone knew that there was no functional (financial) reason for the government to issue debt and that it just transferred public funds into the hands of the speculators then I think attitudes might change.