Hasierarako, ikus Bretton Woods, John Maynard Keynes eta gaurko mundu ekonomikoa

Segida:

(1) DTM-ko jatorri intelektualak

Randall Wray-ren MMT’s Intellectual Origins1

R. Wray: MMT: A Doubly Retrospective Analysis2“…

(a) Hasieraren hasiera3

(b) Atzo goizean, 2011an4

(c) Bill Mitchell5, Warren Mosler6

(d) Mosler, berriz7

(e) Mat Forstater8 (eta Abba Lerner)

(f) Bretton Woods konferentzia (1996)9

(g) Dirua monopolio publikoa10

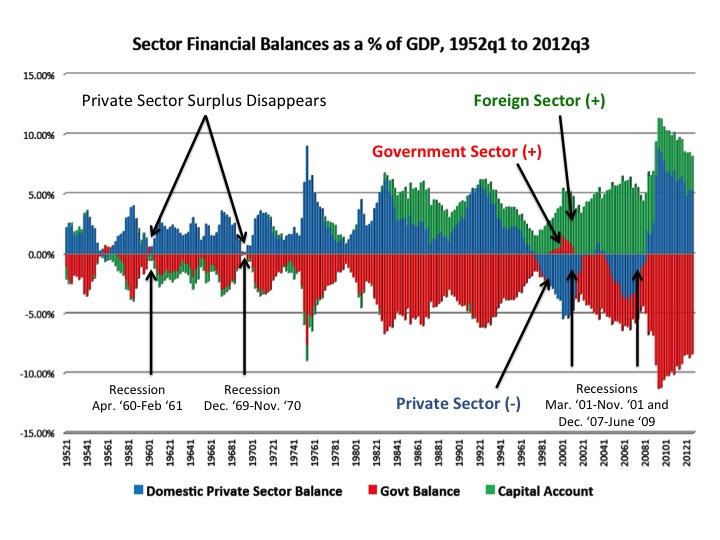

(h) Wynne Godley eta balantze sektorialak11

(i) Eurolandiako balantzeak12

(j) Boterea: desoreka erreala13

Eta ondorioz, Finantza Krisi Globala14.

(2) Soft Currency Economics

Warren Mosler-en Soft Currency Economics (January, 1994)

Pavlina Tcherneva: A Critical Review Of Soft Currency Economics (June, 1996)

Zipriztinak:

(i) Oharra: “When he [ Molser] uses the word “government”, Mosler includes both the Central Bank and the Treasury, as agencies of the government.”

(ii) “Fiat money is a tax credit not backed by any tangible asset15”

“Taxes function to create demand for federal expenditures of fiat money, not to raise revenue per se.”

Gehigarria, Mosler-ek: My response to a post on an Italian Keynes blog16

“Note too that ‘Soft Currency Economics’ was a result of my first hand experience after 20 years in banking and monetary operations. I had never read Keynes, or even heard of Lerner, Knapp, or had any knowledge of any ‘post Keynesians’. So while it may be true that MMT can be derived from one school of thought or another, it didn’t happen that way.(…)”

(3) DTM-ko bilakaera

(z) Randall Wray-k:

“…if you look back to MMP #3017 you will see how I defined MMT as an integration of several approaches to monetary theory, including Chartalism, Endogenous Money, Monetary Theory of Production, Functional Finance, Sectoral Balances Approach, and Circuit Theory. Personally, I’d also add Minsky’s Financial Instability theory and probably a few other bells and whistles.”

Oharra lan bermeaz:

Randall Wray-ek: BIG (Basic Income Guarantee) ala JG (job guarantee)?18

Bill Mitchell: “The reality is that the JG is a central aspect of MMT because it is much more than a job creation program. It is an essential aspect of the MMT framework for full employment and price stability.”

Pavlina Tcherneva: “The JG is not just an afterthought to MMT but a crucial component that has so far offered the most coherent counter-cyclical economic stabilizing mechanism.”

(y) History of MMT and the euro, 1996 Bretton Woods Conference

A FRAMEWORK FOR ECONOMIC ANALYSIS

An Invitational Conference

Bretton Woods, New Hampshire

June 12-15, 1996

The purpose of this conference is to bring together a selected

group of portfolio managers, analysts, researchers

traders, and academics who have a common understanding

of monetary operations.

The objective of this conference is to achieve agreement on the use

of a common conceptual framework for undertaking

contemporary macroeconomic analysis.

Portfolio managers in attendance are responsible for well over

$50 billion19 in assets. The economists and analysts from the

international dealer community represent some of the world’s

largest and most sophisticated fixed income trading and sales

operations.

We believe that this group has the potential to establish an international

standard for the presentation and analysis of economic data.

(x) Soft Currency Economics II

Amazon to publish Soft Currency Economics II

Oct 26, 2012

1 Ikus https://www.youtube.com/watch?v=_I41sfhYvi0&feature=youtu.be. (Ikus hasiera)

3 Ingelesez: “Warren Mosler, Bill Mitchell, and I used to meet up just about every year to count the number of people in the world who understood what we were talking about. I remember just a few years ago at Vail, Colorado, we finally got beyond the fingers on two hands.”

4 Ingelesez: “Now try googling MMT—millions of hits and what is more surprising is that there are blog sites all over the web devoted to MMT, run by people I’ve never heard of. That is a good thing, of course, even if they do not always get things exactly right.”

5 Ingelesez: “And then there was this strange profane guy named Bill Mitchell who swore like a drunken sailor.”

6 Ingelesez: “And one other guy stood out —a hedge fund manager named Warren Mosler who was continually pushing two things. First there was something he called soft currency economics. It sounded to me like good old Keynesian economics from the Treatise on Money, which followed Knapp’s state theory of money.”

And then there was the job guarantee, which I immediately recognized as Minsky’s employer of last resort. I can’t remember what Warren called it but Bill called it BSE, buffer stock employment.”

7 Ingelesez: “What Warren also added was a much deeper understanding of bank reserves and treasury bonds. I came at this from the PK endogenous money, horizontal reserves view of Basil Moore. There’s nothing seriously wrong with that, but it never understood why a sovereign government would sell bonds. Warren explained bond sales as a reserve drain, and lightbulbs went off. Exactly right: government sells bonds to hit the overnight interest rate target.”

8 Ingelesez: “I think it was Mat Forstater who brought the final piece of the puzzle: Lerner’s functional finance approach. I don’t think the basic conclusions were new to any of us, but it was nice to find that a rather mainstream economist reached the same conclusion in the 1940s. Affordability is never a proper concern of a sovereign government.”

9 Ingelesez: “And then he [Mosler] invited me to his conference at Bretton Woods in 1996, where I got to help push MMT onto his hedge fund friends. We began to discuss a bigger project, leading to the creation of CFEPS, which eventually ended up at UMKC with Mat joining and later Stephanie Bell/Kelton.”

10 Ingelesez: “What I want to do today is to argue that both the left and the right as well as economists and policymakers across the political spectrum fail to recognize that money is a public monopoly.”

11 Ingelesez: “Wynne Godley taught us about balances—the sectoral balances. If you take a look at US sectoral balances across the three sectors, what do you see? Balance. A mirror image. … In normal times, the private sector surplus plus the current account deficit equals the budget deficit. In the abnormal times of private sector deficits, we still saw balance—the government even ran budget surpluses for a few years to maintain the balance.”

12 Ingelesez: “Take a look at Euroland’s balances; what do you see? Balance.

Isn’t it amazing? Whenever the private sector surplus rises, the budget deficit rises; the correlation is near 100%, with the current account acting as the balancing item.

Financial balances balance.

If you take the world as a whole, there is no external sector since we don’t trade with Martians. And so the sum of the global government deficits equals the sum of the private sector surpluses. It balances.

What’s the problem in Euroland? Power. Private creditors in central Europe have too much of it; Sovereigns on the periphery have too little.

The creditors are starving the member states, aided and abetted by the Euro, which usurped sovereign power and handed it over the banking elite.

But even still, the balances balance. You can curse the moon for its travels but it still is going to circumnavigate the globe.

Admonish the Mediterraneans all you like for their budget deficits, but they still will have them compounded by the German export surpluses.”

13 Ingelesez. “The real imbalance is power. And this isn’t just a European disease. There is a generalized perception of a world out of balance. We’ve got Arab springs, Occupy Wall Street movements, and protests all over Europe.

Why? Imbalances: everywhere I look in the Western world, the public sector is too small; we’ve privatized too many essential public sector functions—our arts, culture, prisons and punishment, military in Iraq, increasingly our education, our motor vehicle departments. All privatized.

Even responsibility for full employment, and supervision of our banks. We let them self-regulate, and even self-prosecute and self-punish. What happens? Fraud, unemployment, inequality, poverty, and inadequate healthcare, retirement, and welfare.

If you think about it we chose the worst of all possible times to embark on the great Neoliberal experiment—downsizing government, privatizing many of its functions, slashing the safety net. In the West we are aging—which creates the twin problems of the need to devote more resources to aged care and at the same time a private desire to accumulate financial resources for individual retirements.

And that in turn led to the accumulation of unprecedented financial wealth under management by professionals.

Current and future retirees demand higher returns to increase their security and what Minsky called Money Manager Capitalism responded by pouring more resources into the financial sector, doubling its share of value added and capturing 40% of all corporate profits.

It’s too much. Finance is at best an intermediate good that might in the best of circumstances contribute to production. At the same time, financial wealth represents a potential claim on output but does not guarantee output will be available as needed.

We need old folks homes but finance is more interested in gambling on CDOs squared and cubed.

But it is worse than that. Modern finance, at least what is practiced at the biggest banks, is about fraud.

So finance is not even a zero sum game—it largely makes a negative economic contribution.

So the imbalance is one of power. The disease is money manager capitalism. The symptom is the subprime frauds in the US, the austerity imposed on Greece and Ireland, the stagnation of incomes in most developed nations, the rising inequality and poverty in the midst of plenty, the growing despair and feelings of hopelessness.”

14 Ingelesez: “We are headed into another Global Financial Crisis, and likely into a Great Depression 2.0. We’ve handed the monopoly power over to Wall Street and tied the hands of government.

The Occupy Wall Street protestors have got it right—you’ve got to cut off the head of the beast—the Blood-Sucking Vampire Squid on Wall Street that has completely subverted democracy.

We must have fundamental reform and MMT shines a light on the path we need to take.”

15 Honela dio Tcherneva-k, ingelesez: “To fully grasp this concept consider the process of monetization of African colonies with the currency of the colonial power. African communities that were engaged in subsistence production and internal trade had no need for European currency. Walter Rodney reports on a widespread practice employed by the colonial powers to force Africans to use their currency:

In those parts of Africa where land was still in African hands, colonial governments forced Africans to produce cashcrops no matter how low the prices were. The favourite technique was taxation. Money taxes were introduced on numerous itemscattle, land, houses, and the people themselves. Money to pay taxes was got by growing cash crops or working on European farms or in their mines. (Rodney, 1972, p. 165, original emphasis)

The British and other colonial powers, interested in African produced cash crops and wage labor, refused to accept inkind payments, instead imposing taxes payable only in their own currency. This turned out to be a highly effective means of compelling Africans to enter cash crop production and to offer their labor services for sale. In addition, as the only local source of British pounds, the colonial authority was also in a position to determine the price it would pay for those goods and services. In his book, A Political Economy of Africa, Claude Ake also stresses this process of monetization of African colonies:

African economies were monetised by imposing taxes and insisting on payments of taxes with European currency. The experience with paying taxes was not new to Africa. What was new was the requirement that the taxes be paid in European currency. Compulsory payment of taxes in European currency was a critical measure in the monetization of African economies as well as the spread of wage labor. (Ake, 1981, pp. 3334)

It is clear that the imposition of the colonial monetary system in African colonies relied heavily on this method of taxation. Samir Amin (1976) echoes this view point. Amin argues that competition was not essential for the vitality of the African village community as it was in the transition from feudalism to capitalism in the west. “Monetarization of the primitive economy” was thus seen by the colonial powers as an important step in the incorporation of Africa and her resources into the emerging global capitalist system. According to Amin, the most prevalent method of ensuring this goal was placing upon African peoples “the obligation to pay taxes in money form” (ibid., 1976, p. 204).

These examples illustrate how African colonies were monetized. Recognizing that the clever colonial Governor could have just as well used his own script rather than British pounds, we reinforce Mosler’s analysis, the “family currency model”. In this model the parent plays the role of the government and wants the children to do certain household chores. To accomplish this, the parent has decided to offer his or her business cards as payment for completed chores. Initially, however, the children have no incentive to accumulate those business cards and are not thereby motivated to do the desired household chores. However, as soon as the parent imposes a head tax for living in the house, payable only in business cards, demand for the cards is created and chores begin to get done.

The examples of African colonies and Mosler’s “family currency model” illustrate that fiat money begins with a tax. The US government, for example, imposes taxes and requires by law that they are paid in dollars. The underlying reason why the government’s dollar is accepted is because it is needed to pay tax obligation.

Mosler concludes:

“Taxes function to create demand for federal expenditures of fiat money, not to raise revenue per se.”

19 Bilioi amerikar bat = mila milioi europar.