(i) Michael Roberts-en More momentum on the banks:

(https://thenextrecession.wordpress.com/2018/09/25/more-momentum-on-the-banks/)

At the weekend, I participated in a session on what to do about the banks at the Momentum conference (The World Transformed) in Liverpool, England. For those readers who do not know what Momentum is, it is a campaigning group within the British Labour Party that supports more radical measures in favour of labour and backs the current leftist leadership in the Labour Party of Jeremy Corbyn. The Momentum conference takes place alongside that of the official Labour Party Conference and complements it with debates, discussions and events.

The session on banking took place at the same time as Corbyn was speaking with other big names in a separate session. (…)

(…) Labour leaders adopted ‘light touch regulation’ of the banks, praising the City of London. When Chancellor, in 2004 Gordon Brown even opened Lehman Bros’ new Canary Wharf office, saying “Lehman brothers is a great company that can look backwards with pride and look forwards with hope”(!). As we know, the bankruptcy of this rapacious American investment bank was the trigger for the global financial meltdown. And it seems, said Wrack, that even now the current trade union and Labour leaders are unwilling the grasp the nettle and deal with the big banks.

Fran Boait of Positive Money spelt out how ‘neo-liberal’ pro-market ideas dominated thinking on finance. Mainstream economists did not see the global financial crash coming and on the whole have not offered any real changes, except to suggest more capital backing for banks. Positive Money campaigns for “an economy that isn’t driven by housing bubbles, stock market booms, and a bloated financial sector and where wealth isn’t concentrated in fewer and fewer hands. Instead, investment in productive sectors of the real economy, such as affordable housing, helps to boost incomes, bring down inequality and serve society’s needs.”

Ann Pettifor is a well-known UK-based analyst of the global financial system, director of Policy Research in Macroeconomics (PRIME) a network of economists concerned with Keynesian monetary theory and policies; an honorary research fellow at the Political Economy Research Centre at City University, London (CITYPERC) and a fellow of the New Economics Foundation, London. She is an important adviser to the current Labour leadership on economic policy. Ann argued for the Bank of England to be brought under democratic control and then used to provide funds for the big banks as long as they were committed to use it ‘productively’ in investment and jobs etc. This would go alongside the current Labour proposal for a National Investment Bank (NIB).

In my view, none of these approaches is likely to deliver what we need: namely, turning banking into a public service for the many and not a speculative, tax evasion tool for the few rich investors and corporations. Surely, the history of the period leading up to the global financial crash – the wild credit boom, the sub-prime mortgage crisis, the ‘toxic’ derivatives etc – has shown that the big banks will not be a public service without them being publicly owned with democratic accountability. And the period since (the last ten years), only confirms that view.

In my contribution, I outlined briefly how the big banks even after the end of the global crash and the bailouts, have carried on just as before – it’s business as usual. Or as Lloyd Blankfein, the head of Goldman Sachs, the world’s most predatory investment bank, once said: they continue to do “God’s work”. And what has doing God’s work entailed over the last ten years? A never-ending litany of scandals – particularly by British banks.

Take RBS, Britain’s largest bank, partly nationalised after the crash. Before the crash, it was run by ‘Fred the Shred’ Goodwin (so named for his penchant for slashing lower ranked banking jobs and bank branches). Sir Fred Goodwin was knighted for his “services to the banking industry” by the then Labour government. He was noted for his bullying of staff and his love for risky ventures and huge bonuses. After driving RBS into near bankruptcy in the crash, he left, but not without taking a fat pension and handshakes from the RBS board, as have all the senior executives of the banks when they have been asked to ‘step down’ following a scandal.

After the crash, RBS was prominent (while still part nationalised) in the notorious Libor-rate rigging scandal, where bank traders colluded to fix the interest rate for inter-bank lending. Libor sets the floor for most loan costs across the world. That rigging meant that local authorities, charities and businesses ended up paying billions more than they should for loans. The rigging activities of RBS appeared to have been even worse under the ‘watchful’ eye of Stephen Heston, appointed when the bank was nationalised. For two years after Heston got the job, the Libor traders in this publicly-owned bank carried on rigging the rate knowing it was illegal.

Then there is Britain’s next biggest bank, Lloyds Bank (also part nationalised), which took over the scandal-ridden Bank of Scotland in the crash. Along with all the other banks, it has had to compensate customers for mis-selling them personal injury insurance to the tune of £5bn.

During the crash, Barclays Bank was run by Bob Diamond. It has now been revealed that when Barclays was threatened with partial nationalisation, the Barclays board loaned money to Qatar who then invested in the stock of the bank to the tune £12bn. In this way, the bank avoided state control by issuing more loans for equity. It is still not clear what “commissions” were paid to Qatari investors.

And then there is HSBC. In the US, HSBC was fined $5bn by the Federal authorities for ‘laundering’ money for Mexican drug cartels! In Switzerland, former chairman, Stephen Green, was also doing ‘God’s work’ for HSBC. Reverend Green, an ordained vicar, published Good Value in 2009, an extended essay on how to promote ‘corporate responsibility and high ethical standards in the age of globalisation’! The good Reverend was in charge of HSBC’s private banking division based in Switzerland. The Swiss division was engaged in hiding the ill-gotten gains of thousands of rich people in many countries who did not want to pay tax. HSBC arranged various schemes to enable these rich people to recycle their cash back to the UK and other countries without tax payments.

Indeed, tax evasion is just what privately-owned, not democratically accountable banks get up to: providing tax avoidance and evasion for very rich people and corporations. Take the very latest scandal emerging from Danske Bank, Denmark’s largest. After the global crash up to 2015, Danske’s Estonian branch laundered over $200bn of Russian and British corporate cash to avoid tax. UK corporate entities were the second-biggest proportion of customers, behind the Russian mafia, of 15,000 non-resident customers at the Estonian branch of Danske. making it one of the biggest money-laundering scandals ever. Surely we cannot let this continue?

A proper banking service should take our deposits, look after our savings and offer loans to households and small businesses for big ticket items at reasonable interest rates. But the current banking system is much more interested in speculating in financial markets for big bucks, making corporate finance deals and helping the rich evade payments; while top executives take home huge wages, bonuses and pensions.

Britain’s banks cannot even do the basics properly, because they do not spend enough on their staff and systems. There has been a stream of outages and failures in internet banking systems. As current Conservative minister, Nicky Morgan put it: “It simply isn’t good enough to expose customers to IT failures, including delays in paying bills and an inability to access their own money. High street banks justify the closure of their branch networks on the basis that they are providing a seamless online and mobile phone banking service. These justifications carry little weight if their banking apps and websites cannot be relied upon.”

As for providing credit for productive investment in the economy; it’s a joke. In our report for the FBU we calculated that less than 6% of bank assets go to industry for productive investment. The big five British banks control 60% of all lending; their firepower for investment is much greater that Labour’s proposed NIB will ever have. But the big five banks do not use that credit productively. The NIB will not succeed in turning the British economy around if the big five continue to do ‘God’s work’. Instead, another financial crash and recession is more likely.

So public ownership of the big five is essential. Even if the government bought all the shares at market price it would cost only a one-off 3% of GDP (not that full compensation to shareholders is merited). That could easily be financed by the issuance of government bonds and serviced easily with the revenues and profits from the big five. The top executives of these banks would then be paid civil service salaries and have no shares – bank workers and trade unionists would sit on the boards to ensure accountability. Public ownership does not mean more bureaucracy – on the contrary, it means more democracy.

What can public service banks do? Well, take the example of North Dakota. The main bank in this right-wing US state has been publicly owned since the Great Depression. It looks after the deposits of customers and provides loans for households and farmers, and any profit it makes goes back to the state government. It does no speculation and no laundering. It did not suffer during the global crash.

As for investment, take the role of China’s state banking system. Whatever we might say about the autocratic, one party dictatorship in China, its state-owned banks provide credit to support a national investment programme that has transformed China’s infrastructure. I came up to Liverpool on one of Britain’s privatised train routes. It left one hour late because of ‘engineering works’and crawled up to Liverpool at a maximum speed of 75mph. On the same day, China launched a new high-speed service (220km/h) from Hong Kong to China linking it with 15 cities: punctual, modern and cheap. This high-speed rail service reduces the need for air flights and lowers the carbon footprint. And all this was financed by state bank loans and railway bonds.

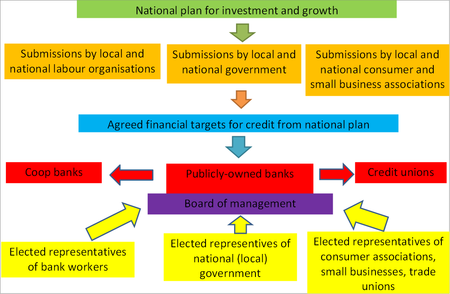

It was argued at the Momentum session by Fran Boait and by several in the audience that we don’t want great big bureaucratic banks but more diversification: regional banks, coops, credit unions etc. I agree. Germany’s banking system is predominantly state-owned at regional level with savings banks and development banks. Linking the nationally owned big five with such regional and local banks would be the way to go. Indeed, I have even drawn up a plan for such a banking system.

But this will only work if we have the core of banking in public hands. If diversification means keeping the big five still owned by capital with just small banks and credit unions around the periphery and/or competing with the big five, then that would be like saying the health service should have at its centre big private health companies with only small public operations in the community.

There seems to be a reluctance to opt for public ownership at the centre of the banking system. Why only railways, energy and water? The lack of momentum on this crucial cog in controlling the economy for the many not the few seems be partly based on fear of the media and the City of London’s response. But breaking up the banks or taxing them, or giving workers shares in the banks as Labour’s finance leader John McDonnell is now proposing will provoke just as much antagonism from capital – but without delivering banking as a public service and a force for productive investment.

I don’t quote Lenin very often. But he hit the nail on its head (as he often did), when he said: “The banks, as we know, are centres of modern economic life, the principal nerve centres of the whole capitalist economic system. To talk about “regulating economic life” and yet evade the question of the nationalisation of the banks means either betraying the most profound ignorance or deceiving the “common people” by florid words and grandiloquent promises with the deliberate intention of not fulfilling these promises.”

Mon dieu! Lenin!

(ii) Gehigarria bankugintzaz:

Aurreko guztia ikusita, gogoratu behar da aspaldian Randall Wray-k idatzi zuena, baita emandako irtenbideak ere:

Eta sistema osoak, berriz ere, krak egingo balu?

Bankugintza eta diruaren gaineko kontrola

Randall Wray-k Bernie Sanders-ez

Oro har, hona hemen bankugintzaz UEUko blogean azaldu dena:

Ezjakintasunetik, Libera nos domine!