Hasteko, ikus Gutxieneko alokairua eta lanpostuak (Mosler-Silipo-ren proposamena)

Segida:

Albistea: Stabilità dei prezzi e disoccupazione le soluzioni di Mosler al Festival per l’Economia1

(a) Damiano Silipo-k ikerketa berri baten emaitza eman du, politika monetarioaren tresna berri bat aurkeztuz2

(b) Ikerketa Silipo eta Mosler-ek egin dute: Maximizing Price Stability in a Monetary Economy, Europar Batasuneko tratatuekin ados dagoena, alokairuak eta prezioak erdigunean egonik3

(c) Mosler-en hitzez, langabezia inflazioa aldatuz konpondu daiteke4

(d) EBZ-k lana finantzatzeko plana proposatuz, sektore pribatuko langabeziatik lanpostuak kreatzearren, proposamenak prezioen egonkortasuna mantentzen du5

Ikerketa hauxe da: Warren Mosler eta Damiano B. Silipo (2016) Maximizing Price Stability in a Monetary Economy: http://www.levyinstitute.org/pubs/wp_864.pdf

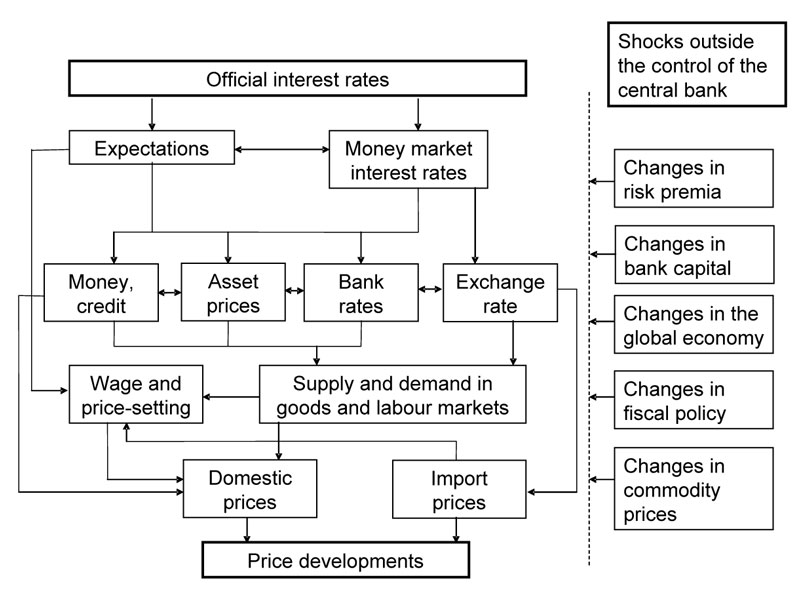

Eduki orokorra, EBZ-ren rola:

“We introduce an additional tool for promoting price stability and conclude that public purpose is best served by the selection of an alternative buffer stock policy that is directly managed by the ECB”

Hona hemen ikerketan ukitutako zenbait zehaztasun:

i) Inflazioaren helburua: %2 ingurukoa izatea6

ii) Mekanismoa

iii) Bi uste7: usteak erdi ustel8

iv) Erabilitako politika desberdinak9

v) Emaitzak ez dira izan espero ziren modukoak10

vi) Alokairu finkoa versus salgaiak edo merkantziak11

vii) EBZ-ren rol nagusia12

viii) EBZ-k orain arte bere politikekin lorturiko emaitza kaxkarrak13

ix) Konparaketak14: “We provide evidence that a labor buffer stock policy is a superior policy in achieving price stability relative to current policy, with respect to both the costs and benefits of monetary policy”

xi) NAIRU versus NRTE15

xii) EBZ-ren rola: mikroekonomiak dioena16

xiii) Politikaren inplementazioa: hasteko alokairua 7€ orduko, 35 orduko astean17

xiv) Kostuak eta mozkinak: zein da trantsizioko enpleguen kostua EBZ-rako?18

xv) Emaitza19: “… a fixed-wage employed buffer stock policy is the unambiguously superior policy option with regard to the ECB’s primary objective of price stability,…”

Bibliografia txikia

Micossi, S. 2015. “The Monetary Policy of the European Central Bank (2002–2015).” LUISSSchool of European Political Economy Working Paper.

Mosler, W., and M. Forstater. 1998. “A General Framework for the Analysis of Currencies and Commodities.” in P. Davidson and J. Kregel (eds.) Full Employment and Price Stability in a Global Economy. Cheltenham: Edward Elgar.

http://www.mosler.org/docs/docs/general2.htm

Tcherneva, P. 2002. “Monopoly Money: The State as a Price Setter.” Oeconomicus 5: 124–43. http://www.epicoalition.org/docs/Pavlina_2007.pdf

1 Ikus http://www.ilquotidianoweb.it/news/economia/746034/Stabilita-dei-prezzi-e-disoccupazione-.html#.VxNk6oMnYb4.facebook.

2 Italieraz: “...Damiano Silipo, sono stati illustrati i risultati di una recente ricerca , incentrata sull’utilizzo di un nuovo strumento di politica monetaria. Il dibattito è subito entrato nel vivo: «La Banca centrale europea – ha esordito Silipo- ha ricoperto bene il ruolo di prestatore di ultima istanza, salvando alcune banche dal fallimento ma non si può dire lo stesso per quanto concerne la capacità di creare crescita e occupazione, tanto che ci troviamo in situazione di deflazione».“

3 Italieraz: “Analizzati gli effetti delle scelte della Bce che, stando al pensiero del docente, non sarebbe riuscita nemmeno a influenzare la variabile dell’inflazione attesa, non producendo, di conseguenza, effetti sull’inflazione effettiva. Lo studio targato Silipo e Mosler “Maximizing Price Stability in a Monetary Economy”, è una proposta compatibile con i trattati Ue e con le attuali funzioni della Bce. Al centro, la determinazione dei salari e dei prezzi, tramite i quali la Bce interverrebbe nell’anello precedente – quello dei salari- influenzando i prezzi.”

4 Italieraz: “ Uno strumento in più, aggiuntivo, come lo ha definito Mosler : «La questione è la disoccupazione, se non fosse all’11 per cento (in Italia) questa sala sarebbe vuota. Il problema dal loro punto di vista (Ue) si risolve variando l’inflazione. L’aumento dei tassi di interesse, farebbe rallentare l’economia e crescere la disoccupazione. Viceversa, se i tassi diminuiscono, l’inflazione aumenta».”

5 Italieraz: “A ciò si aggiungono ulteriori considerazioni concernenti lo status di disoccupato. Le aziende – come più volte sottolineato dall’economista – difficilmente tendono ad assumere disoccupati, perché confortate da lavoratori già inquadrati in contesti lavorativi, maggiormente valutabili. La riserva di disoccupati, dunque, non funziona quando l’economia va bene: «La nostra proposta – ha aggiunto Mosler – prevede che la Bce finanzi un piano di lavoro al fine di aiutare la transazione tra disoccupazione e occupazione nel settore privato, mantenendo piena occupazione e stabilità dei prezzi».”

6 Ingelesez: “Article 127 of the Treaty on the Functioning of the European Union establishes that the primary objective of the European Central Bank (ECB) is to maintain price stability. Other policy goals related to the objectives laid down in Article 3 of the Treaty on the European Union, including “full employment” and “balanced economic growth,” are supported by the ECB but “without prejudice to the objective of price stability.”

While the Treaty does not give a precise definition of what is meant by price stability, the ECB’s Governing Council has clarified that price stability implies maintaining a year-on-year increase in the Harmonized Index of Consumer Prices (HICP) for the euro area below but close to 2% over the medium term.”

7 Ingelesez: “The first is that the ECB mandate—the price level—is a function of interest rate policy. The second is the more general notion that by keeping inflation stable economic activity can be, for all practical purposes, as close as possible to its potential.”

8 Ingelesez: “The macroeconomic developments during the crisis that started in 2007 have brought into question both the primary argument for inflation targeting along with the instruments used by the ECB to pursue their price stability mandate in the eurozone. Additionally, the relationship between unemployment and inflation has been called into question.”

9 Ingelesez: “… to affect prices and output, central banks have experimented with unconventional policies including quantitative easing, targeted easing, negative interest rates, and new forms of liquidity provisioning. On January 22, 2015, for example, the ECB announced a quantitative easing program, including the purchase of at least 1.14 trillion in euro securities over two years, in an attempt to increase the rate of inflation in the euro area from near zero to its target of 2% over the medium term (Micossi 2015).”

10 Ingelesez: “… it does not seem that this program is capable of affecting inflation expectations as were presumed to be required for achieving price stability. Indeed, since the period quantitative easing implementation began in the euro area the gap between the change in the ECB balance sheet and the two years ahead inflation forecast, the EBC’s critical determinant, increased.”

11 Ingelesez: “The aim of this paper is to show first that a buffer stock policy that uses employed labor at a fixed wage as a buffer stock functions as a superior price anchor than a buffer stock that employs commodities. We then show further that an employed labor buffer stock provides a superior price anchor than that achieved by the ECB’s current policy, which utilizes a buffer stock of unemployed labor to stabilize prices.”

12 Ingelesez: “With a buffer stock policy the nominal price of the buffer stock is defined by the state, and in our proposal it would be defined by the ECB per its mandate for price stability as specified in the Maastricht Treaty. Subsequently, market forces result in other prices continuously reflecting indifference levels that express relative value with regard to the value of the buffer stock.

Likewise, with the nominal price of the buffer stock fixed, any change in the relative value of the buffer stock itself is expressed as a change in the nominal price level of all other prices. Therefore the lower the price volatility of the selected buffer stock in the current policy, the greater the expected general price stability when the price of that buffer stock is, in our proposal, fixed by the ECB. On this basis, the employed labor buffer stock is clearly superior.”

13 Ingelesez: “These results suggest that the monetary policy has been ineffective in spurring inflation and growth in the crisis period. Indeed, in this period the ECB mainly played the passive role of providing the liquidity necessary to save distressed banks, rather than an active role in promoting price stability. By contrast, after 2013 the primary target of the ECB has been the fight against deflation in the euro area.

Therefore, utilizing the ECB’s internal methodology, what is the likely impact on inflation and output of the ongoing program of asset purchases by the ECB, taking account also of the latest inflation expectations surveyed by the ECB for the euro area?

The results of the forecasts show that, given the ECB’s own assumptions and the empirical evidence, even if the ECB pursues the current policy of an asset purchase program until the end of 2017 the target inflation rate of 2% is unlikely to be achieved.

More worrisome is the low growth rate of the real GDP forecast, (…) suggesting that current monetary policy is unlikely to bring the euro area out of the present sluggish growth rate.

From the previous analysis, it is straightforward to conclude that, given the data and the ECB’s assumptions, current monetary policy by the ECB is unlikely to lead to price stability in the euro area. This is because in the context of large output gap, presumed inflation expectations, which are further presumed to cause inflation, hamper the achievement of the monetary policy target.”

14 Ingelesez: “In its elemental form an employed labor buffer stock policy is one where the government offers a fixed-wage transitional job to anyone willing and able to work. We call it a “transitional” job because it’s designed to facilitate the transition from unemployment to private-sector employment (note that we further suggest it is arguably not wrong to call this policy a “structural reform” that promotes efficiency and “competitiveness”). In practice, the size of the labor buffer stock would increase as demand for labor in the economy weakens, and the size of the labor buffer stock would diminish as the demand for labor in the economy increases, much like today’s unemployment increases and decreases.

The first beneficial attribute of the employed labor buffer stock versus unemployment is that it is more liquid than today’s unemployed buffer stock policy, and therefore it would provide a superior price anchor in support of the ECB’s single mandate. Additionally it is more supportive of private sector growth in output and employment. The primary reason for this superior labor liquidity and performance versus today’s policy of using unemployment as a buffer stock is that employers prefer to hire people already working rather than hiring those who are unemployed.

Indeed, it would also support the structural changes in the labor market aimed at increasing flexibility in hiring and firing by the private sector. Also, a labor buffer stock establishes the minimum wage private firms may have to offer to workers to attract them. There are several reasons why employers prefer hiring the employed rather than the unemployed: 1) People who have a job are proven to be interested in working; 2) You can’t be sure why the unemployed lost their jobs; 3) The employed will adjust quicker to a new job; 4) An employed candidate has fresher job skills and known work habits (…).”

15 Ingelesez: “This proposal replaces the concept of the natural rate of unemployment with the natural rate of transitional employment (with the ECB utilizing an employed labor buffer stock policy to sustain inflation at its desired level), rather than utilizing an unemployed labor buffer stock, as per current policy.

Furthermore, we conclude that during an expansion with a given inflation target, the level of transitional employment will be less than the level of unemployment would have been had the ECB attempted to achieve its inflation target with its current policy. The difference is due to the greater ease of transition to the private sector and therefore a greater level of employment facilitated by transitional jobs when the economy operates at, for example, today’s targeted 2% level of inflation. In other words, we claim that an employment buffer stock allows the economy to operate at higher levels of non-inflationary output and employment than in the current case where the NAIRU is the target of monetary policy. Moreover and most importantly, a labor buffer stock policy is likely to reduce fluctuations in prices as compared to the current policy due somewhat to the countervailing effects of transitional employment when the private sector slows down, but to a greater extent when the private sector expands and seeks to hire transitional workers rather than unemployed workers.”

16 Ingelesez: “The role of the buffer stock wage as set by the ECB is described by standard microeconomic monopoly pricing theory, where monopolists are the “price setter” rather than “price taker,” with monopolists setting two prices. The first is the “own rate,” which is how their product exchanges for itself. With a currency this is the interest rate, and the ECB, for example, is the price setter of the policy interest rate for the euro. The second price set by monopolists is how their product exchanges for other goods and services in the economy, and this is done by setting the terms of exchange for at least one traded good or service. With this proposal, that price becomes the wage paid to transitional workers participating in the employed labor buffer stock. That is, that wage becomes the numeraire for the currency, with market forces adjusting all other prices so as to continuously reflect indifference levels with the employed buffer stock wage set by the ECB.

The ECB would then use this wage to achieve its inflation target. Leaving the wage constant would promote 0% inflation of final prices, assuming, for example, 0% productivity growth. And, for example, if the target was 2% inflation, the wage could be continuously increased at a 2% annual rate, again assuming 0% productivity growth. With higher productivity growth, the transitional job wage could be increased by that much to achieve the same increase in final prices.

At the same time, while the wage of the transitional job determines the rate of inflation, it is also critical to manage the size of the buffer stock to ensure it functions as an effective price anchor without prejudice to other aspects of public purpose. Therefore, the ECB would be minding the size of the employed buffer stock as well as the wage. If the size was deemed to be larger than needed to be an effective price anchor, the ECB has the mandate to enact policy designed to increase GDP, which we suggest could include options to accommodate fiscal expansion of the member nations. Likewise, if the size of the employed buffer stock was deemed to be too small to function as a price anchor, restrictive policy would be in order.”

17 Ingelesez: “We begin by setting a non-disruptive wage of €7 per hour for a 35-hour per week transitional job for anyone willing and able to work. We then further propose that the member nations first go to their various ministries and departments and announce that they have unlimited budgets to add any person willing to work as transitional job workers at the prescribed fixed rate of pay. These people could work as assistants in the police departments, educational facilities, and any of the various administrative offices. They would not be meant to displace “normal” government workers to save costs. After 30 days we would extend this program to the various regional governments and city governments, and 30 days later extend the program to non-profit and charitable organizations. This would allow the unemployed seeking paid work to be able to find it regionally, and this makes them more attractive to private-sector employers.

The organization, monitoring, and evaluation of this labor buffer stock policy could be implemented interactively between member countries and the European Commission in a similar way to which current structural policies are implemented, but maintaining ECB independence to establish the terms and conditions of the employment of the transitional workers as well as the authority to monitor the policy for fraud and abuse.

Additionally, we recommend that the transitional wage initially be set at a non-disruptive level, so as not to cause workers already employed to leave their current employment in favor of the new transitional job. This prevents the transitional job from creating an initial, inflationary wage shock that might adversely disrupt commercial arrangements and what’s generically called the “competitiveness” of the business community. And while the transitional job wage does function as a general wage floor, initially setting it at a non-disruptive level subsequently works to prevent deflation while not promoting inflation. This also means that the transitional job wage offered to anyone willing and able to work, as a point of logic, obviates the need for minimum wage legislation.

Again, and as previously described, should the ECB desire to promote, for example, a 2% rate of inflation and again assuming 0% productivity growth, the transitional job wage can be increased 2% annually from its initial setting. “

18 Ingelesez: “The aim of this section is to shed some light on the possible costs of a labor buffer stock policy and the likely effects of this policy on inflation and real GDP growth in the euro area. What would be the cost for the ECB to implement such a program of transitional jobs? The direct cost is related to two indicators: the minimum wage fixed by the ECB, and the number of workers involved in the transitional jobs. Currently, the minimum monthly wage in the euro area countries ranges from €300 in Lithuania to €1,500 in Belgium and €1,923 in Luxembourg. As before, assume the ECB establishes transitional jobs requiring 35 hours per week at a salary of €7 per hour. The ECB or the member countries would bear the cost of implementation of the program. However, there are additional costs the ECB or the member countries would bear in implementing the program. These additional costs are related to the expenditure on new equipment and other capital and intermediate goods necessary to support the transitional workers. In October 2015 in the nineteen countries of the euro area there were 17,240,000 unemployed people. Assuming all the unemployed would like to work at this wage, the maximum direct cost for the ECB to implement this policy is €18.14 billion per month. In the euro area, an individual country’s government expenditure on gross capital formation is about 11.34% of total public expenditure. Assuming the same proportion between capital and labor holds also for this program, it follows that we must add a monthly expenditure of €2.1 billion for new equipment.

However, transitional jobs would allow the euro area countries to immediately save €12.3 billion per month on income maintenance and support expenditures currently being spent on those opting for transitional jobs. This savings, net of the additional capital expenditure, would be remitted to the ECB, thereby reducing gross ECB expenditures for the transitional jobs.

Therefore, the total expenditure for implementing the transitional job program would be about €8 billion per month (€18.14–10.2 billion).

Next we estimate the impact of €8 billion per month by the ECB on nominal GDP in the euro area.

In the first quarter of 2016, the increase in nominal GDP is equal to €24 billion, which is the net amount necessary to implement the program. In the subsequent period, the ECB expenditure is the same, but the nominal GDP continues to increase due to the multiplier effect.

(…)

The results of the forecast show that the expense of funding an employed labor buffer stock policy by the ECB would result in a rate of inflation that hits a high of slightly over 2% before falling back under 2%, and settling back to 1.65% after approximately three years. That is, even with the aggressive assumptions, there is no evidence that the expense of an employed labor buffer stock program would generate unwelcome inflation.

Moreover, with less aggressive assumptions regarding the size of the multiplier, as well as our assertion that an employed labor buffer stock policy is a superior price anchor to today’s unemployment policy, the model would show even lower inflation as a result of the ECB’s net funding of the transitional jobs. “

19 Ingelesez: “We conclude that a fixed-wage employed buffer stock policy is the unambiguously superior policy option with regard to the ECB’s primary objective of price stability, as described in Article 127 of the Treaty on the European Union. Incidentally, this policy contributes to the achievement of the objectives of the Union as laid down in Article 3 of the Treaty on the European Union. Specifically, we propose that the ECB adopt an employed buffer stock policy to optimize compliance with mandated objectives.

(…)

Are gehiago, “Enacting the transitional job for anyone willing and able to work, without prejudice to price stability, also delivers additional benefits, including eliminating the need for minimum wage legislation and the improvement of the quality (as well as quantity) of public-sector services.

Employed as transitional workers, those previously unemployed will be maintaining and enhancing their human capital in the process of working and producing useful output. This is in sharp contrast to the deterioration of human capital during periods of unemployment.

Finally, we stress that this plan is qualitatively very different from a policy that aims to guarantee a minimum income be paid to every citizen. Indeed, what are called “basic income” proposals risk functioning as the antithesis of a price anchor. Those policy proposals do not require beneficiaries to sell their time (work) to earn their compensation, and therefore projected outcomes are entirely different. “

joseba says:

What about the FED?:

It must be impossible for the Fed to create inflation

http://moslereconomics.com/2011/11/14/it-must-be-impossible-for-the-fed-to-create-inflation/

“In conclusion, theory and evidence tell me it’s impossible for the Fed to create inflation, no matter how much it tries. The reason is because all the Fed does is shift dollars from one type of account to another, never changing the net financial assets held by the economy. Changing interest rates only shifts dollars between ‘savers’ and ‘borrowers’ and QE only shifts dollars from securities accounts to reserve accounts. And so theory and evidence tells us not to expect much change in the macro economy from these primary Fed tools, making it impossible for the Fed to create inflation.”