(i) Euroa

The Euro is a failure1

(a) Failure to create fiscal authority

… deceased British economist Wynne Godley got it right in 1992 when he wrote about “Maastricht and all that”

“… the Maastricht Treaty was framed. It is a crude and extreme version of the view which for some time now has constituted Europe’s conventional wisdom (though not that of the US or Japan) that governments are unable, and therefore should not try, to achieve any of the traditional goals of economic policy, such as growth and full employment. All that can legitimately be done, according to this view, is to control the money supply and balance the budget…

…It should be frankly recognised that if the depression really were to take a serious turn for the worse – for instance, if the unemployment rate went back permanently to the 20-25 per cent characteristic of the Thirties – individual countries would sooner or later exercise their sovereign right to declare the entire movement towards integration a disaster and resort to exchange controls and protection – a siege economy if you will.”

(b) Currency weakness

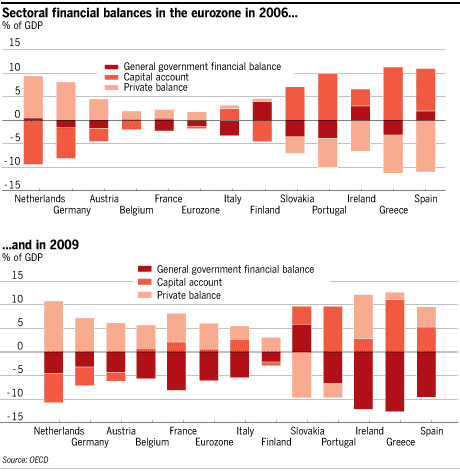

Former Fed Chair Ben Bernanke called the Germans out on this in Apr, …

(c) Lack of intra-eurozone Harmonization

(d) One size fits all monetary policy

(e) Banking system fractured

(f) Monetary financing failure

(g) The resignations at ECB represent failure

(ii) Florentzia (1427-2016)

How to Stay Rich in Europe: Inherit Money for 700 Years2

The richest Florentine families in 1427 still are: New research shows Europe leads the world in inherited wealth.

(iii) Italexit

le probabilità di euroexit dell’italia nei prossimi 12 mesi sono ai massimi storici: bloomberg – h/t @Tcommodity

2016 abu. 23

(iv) Liburua

The financial system and the economy4

Principles of money and banking

(v) Bail-in

Albistea: La proposta della Germania: bail-in anche per i titoli di Stato5

Definizioak:

Bail-out (orain arte oso ezaguna)6

Bail-in (hemendik aurrera ezagutuko dena)7

“… Non è tardi però per avvertire almeno il prossimo «fischio», perché riguarda un tema per l’Italia anche più delicato: il debito pubblico e l’ipotesi che i termini di rimborso sui titoli di Stato vengano fatti slittare e poi drasticamente rivisti al ribasso. La proposta arriva dall’establishment di politica economica tedesco, a un livello avanzato di dettaglio, e applica agli Stati lo stesso approccio che domina la direttiva sui salvataggi bancari. L’idea di fondo è creare un meccanismo semiautomatico per far sopportare ai creditori parte delle perdite di una crisi di debito pubblico, in modo simile a come con il «bail-in» si colpiscono gli investitori quando una banca ricorre all’aiuto dello Stato.

«Un meccanismo per regolare la ristrutturazione dei debiti sovrani» è il titolo del documento di lavoro che nel cuore dell’estate il Consiglio tedesco degli esperti economici ha fatto comparire sul proprio sito. Questo organismo dei «cinque saggi» nominati dal governo di Berlino ha il compito di valutare le politiche economiche in Germania; sempre più spesso però agisce anche da influente fabbrica di idee per il ministro delle Finanze Wolfgang Schäuble.”

(vi) Joan Robinson8

Stephanie Kelton @StephanieKelton9

Minsky referencing Joan Robinson.

2016 abu. 25

2016 abu. 25

(vii) 1998ko maiatzaren 5ean. Warren Molser

Stephanie Kelton @StephanieKelton10

Talk about nailing it. May 5, 1998 @wbmosler

2016 abu. 26

2 Ikus http://www.bloomberg.com/news/articles/2016-08-23/how-to-stay-rich-in-europe-inherit-money-for-700-years.

5 Ikus http://www.corriere.it/economia/16_agosto_24/proposta-germania-fc0d8b8c-6a2c-11e6-a553-980eec993d0e.shtml.

6 A bail-out is a colloquial term for giving financial support to a company or country which faces serious financial difficulty or bankruptcy: ikus https://en.wikipedia.org/wiki/Bailout.

7 A bail-in is rescuing a financial institution on the brink of failure by making its creditors and depositors take a loss on their holdings. A bail-in is the opposite of a bail-out, which involves the rescue of a financial institution by external parties, typically governments using taxpayers money: ikus http://www.investopedia.com/terms/b/bailin.asp.

8 Joan Robinson-i buruz, ikus Joan Robinson eta Joan Robinson-en eskutitz irekia.